How does the war in the Middle East impact our investment outlook plus Q1 2026 portfolio and thematic review

Kirill Pyshkin

Apr 12, 2026

Source: The Economist cover 09.04.2026 edition

The super defensive stance that we advocated at the beginning of this year in our 2026 investment outlook with half of our portfolio invested in gold or hedged to CHF has worked out well so far.

Overall, in Q1 2026 our multi-asset portfolio was slightly up +0.2% in USD terms. We also expected a reversal of USD/EUR sell-off and this was indeed the case as USD has strengthened in Q1 over EUR.

Finally, we called for a conservative equal allocation between equity and bonds, with a preference for longer term US treasuries since the middle of last year. So far this year bonds outperformed equities, and US bonds were the best performing among them.

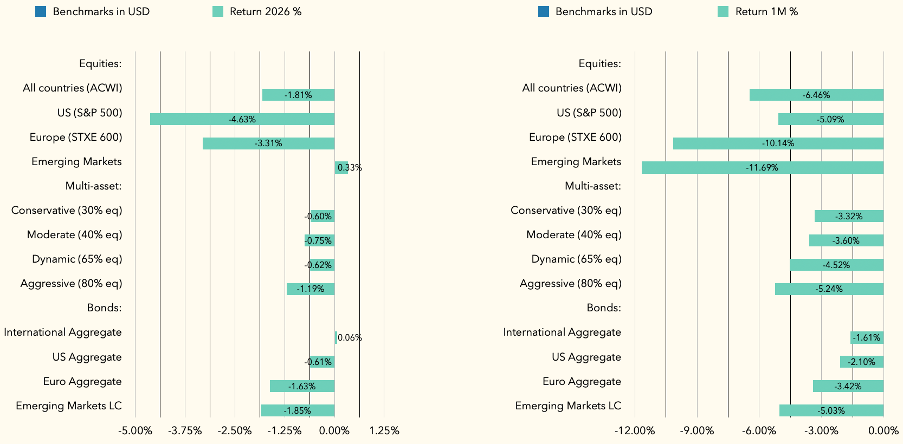

Benchmarks performance 1Q 2026 and in March 2026

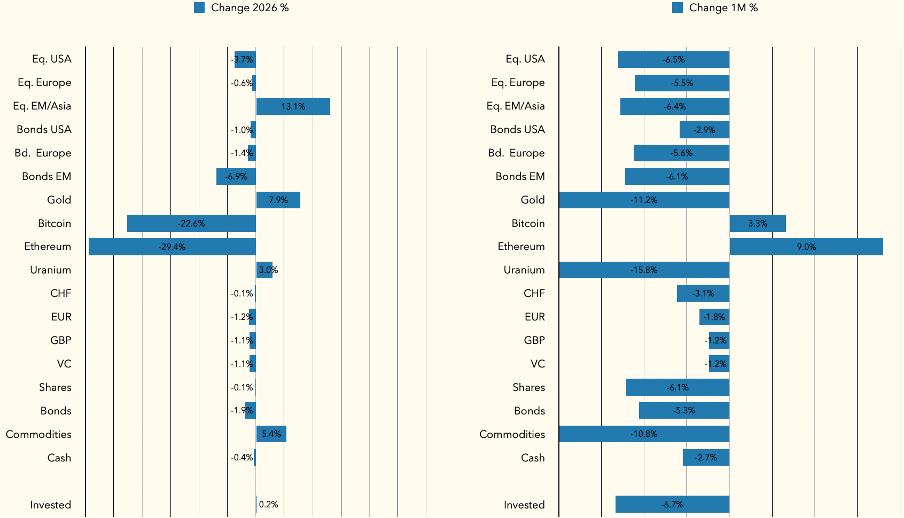

Our multi-asset strategy portfolio performance 1Q 2026 and in March 2026

Our equities selection was down only -0.1%, significantly better than the -1.8% for the world equities benchmark because we had much better selection in Europe and Asia – significantly outperforming regional benchmarks. US equities were the most resilient through the conflict, but our European selection was significantly better than the benchmark and outperformed our US selection.

Our bonds selection was down -1.9%, slightly worse than the benchmark. Our European bonds selection was better than the regional comparison, but our US and emerging markets local currency bonds performed worse, because we underweight Chinese bonds, which proved to be the most resilient. But generally US bonds outperformed European bonds as we expected.

The Middle East conflict impact on the markets

The sell-off in risk assets earlier this year was initially led by crypto and expensive US tech equities. The war in the Middle East has accelerated this sell off and extended it to Europe and Asia, although EM equities remained in the positive territory throughout the conflict while crypto reversed its decline.

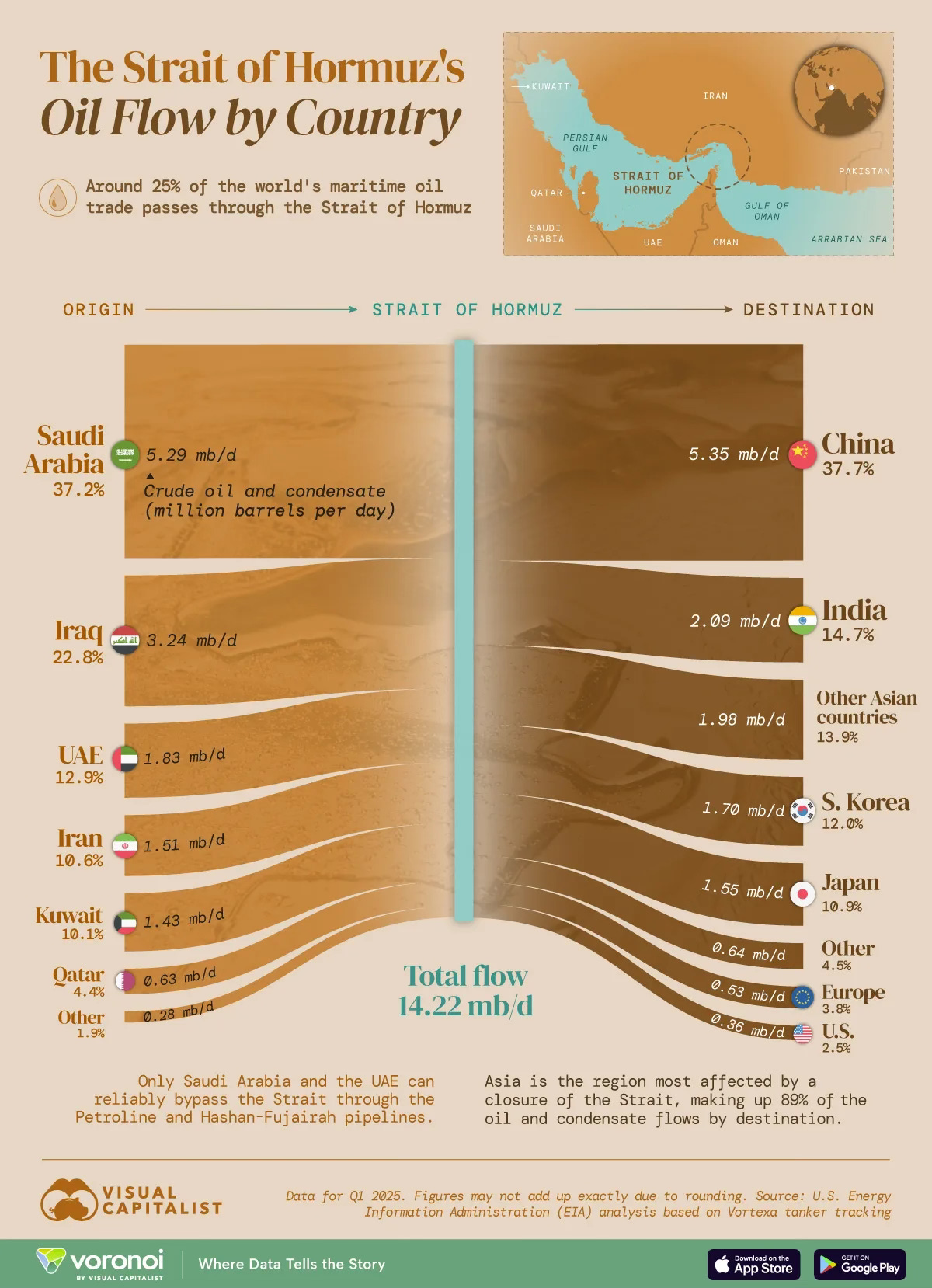

Given the blockade of the Strait of Hormuz, a major oil supply route has been disrupted, which led to an immediate spike in oil price – a key component to manufacturing costs of most goods, and therefore inflation – hence the hit to bonds. Europe and Asia heavily rely on imports of oil and gas from the Middle East, therefore the impact is larger there.

Source: Visual Capitalist Q1 2025

On the other hand, shares in European luxury companies, for example, have been hit hard as these are discretionary items, where sentiment is already negatively affected by wars, plus in this conflict their manufacturing costs are linked to the rising oil price, where Europe is in a particularly difficult place.

Conversely, any sign of peace is greeted ecstatically by the markets with immediate drop in oil prices and the corresponding rally in equity markets, especially in Europe and Asia, where Asian equities generally rally even more. At the same time, bond yields fall on the expectation of lower inflation, again more in Europe and even more in Asia.

No traditional hedge, not even gold

The fact that bonds and equities move together through the roller-coaster of this oil crisis, is bad news for asset allocation, because they don’t provide any hedge against each other as they are expected to do in a multi-asset portfolio.

Even gold, which should theoretically rise in value with any conflict, and in particular the one that incites inflation, did not perform as it should, instead falling by over 10% through the month of March (although it is still positive for the year).

This is especially worrying for the allocators, and may be an indication that gold has become a speculative asset for retail investors, given its stratospheric rise over the last couple of years, rather than a hedge in a multi-asset portfolio. Then it would be the case of profit taking of the biggest winners and momentum trades.

Another surprise was that cryptocurrencies, a purely speculative asset, was the only investment appreciating at least in our portfolio through the flaring of the conflict. Historically, crypto was perceived as an ultra-high-risk investment, hence the expectation that it should sell off first in any risk-off trade, like wars. Was that simply a relief rally after a heavy sell-off in the prior months or a new trend?

What next?

The question now as the peace settlement is hopefully near is what next for the markets. The markets have been fooled several times by the suggestions that the peace agreement is near and someone made a lot of money on those trades.

Can the damage be simply undone and the world returns to where it was a year ago with ships passing freely through the Strait of Hormuz?

Unfortunately, there seem to be a significant damage to the oil and gas infrastructure in the region, which may take long and is expensive to repair. In particular, to the Qatar LNG capacity, which is a significant supplier to the market.

Source: CNN News

Especially Europe, which has tried to ween itself off the Russian gas, now finds itself heavily dependent on the US for supplies, and is paying the full price for that. In Asia, many customers would have secured significant long-term Australian LNG suppliers much earlier, as they never had the luxury of the cheap piped Russian gas.

Source: European Gas Hub

Europe, therefore, from the point of view of energy and, hence, manufacturing costs over the long term will be at a strategic disadvantage even against Asia, let alone US where the energy prices are already much lower.

Nuclear energy could offer a solution if Europe can overcome its historical resistance to nuclear and overturn the ban in Germany. France has the expertise and even former German nuclear operators still exist. European industrial giants are able to supply all the equipment, while Germany has allocated significant spend to infrastructure last year.

Another solution could be re-rapprochement with Russia and lifting the self-imposed sanctions on energy supply. This should come when the conflict in Ukraine is finally settled and European markets are likely to rally on any such announcements. In fact, the EU has already delayed the introduction of the previously envisaged full ban on the Russian oil imports.

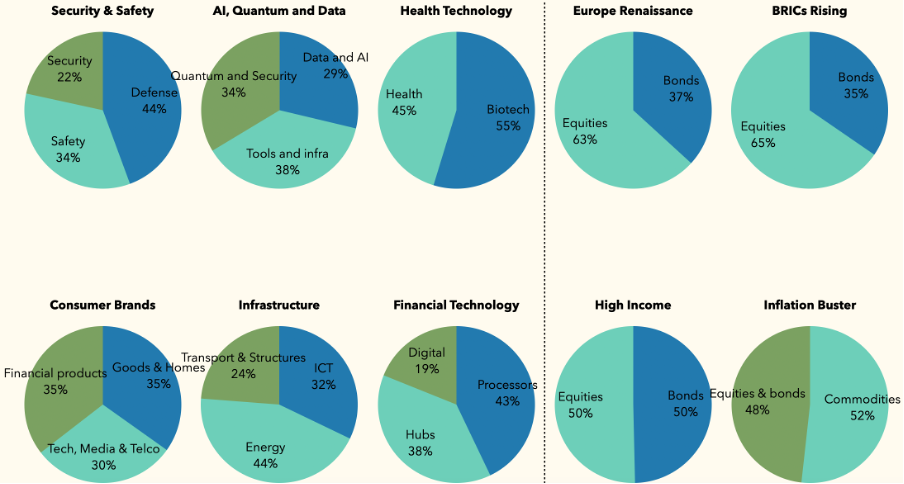

Where to invest thematically?

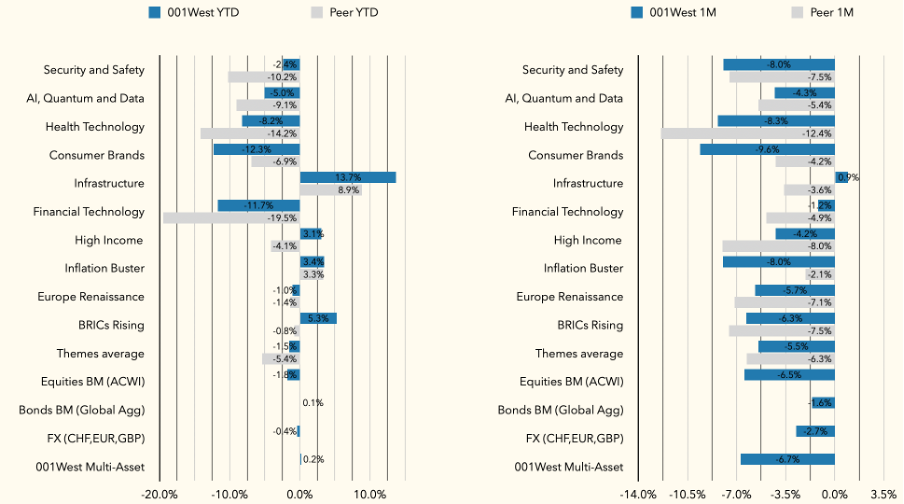

Thematically, at the beginning of March we said that we particularly like the following multi-asset themes: Infrastructure, Inflation Buster and Rising BRICs plus Quantum Tech venture capital. The former three thematic portfolios and also our High Income multi-asset portfolio were indeed the only ones in the positive territory at the end of March.

Our thematic multi-asset portfolio performance 1Q 2026 and in March 2026

Looking at the specific impact of the war in the Middle East:

· Infrastructure disproportionally benefits because a large part of this portfolio is energy infrastructure, which is being destroyed in the Middle East and it will take time to rebuild. Generally, access to infrastructure, including oil and gas, data centres and now bridges and roads destroyed during wars is in high and rising demand around the world.

· Inflation Buster benefits because this war is inflationary in nature as energy is the key component to manufacturing costs. A significant part of this portfolio is gold which did not behave as expected, but we hope this was temporary profit taking phenomenon. Structurally demand for gold is still rising, driven to a large degree by the buying of the central banks, and in particularly China.

· Rising BRICs. Asia is heavily dependent on the Middle East oil, but in our portfolio a significant part is invested in Brazil, which is an oil exporter. Also China and India have an unaffected supply of the Russian oil and gas, and purchasing now has become easier with some US sanctions temporarily lifted.

Separately, our Quantum Technologies VC portfolio, is not marked to market daily as the rest of our multi-asset investments, hence the valuing is more difficult. However, it is 100% UK and the UK government in March announced a record-breaking £2BN funding to become the first country to deploy quantum computers at scale by 2030s. This makes us even more positive on that thematic, with our portfolio companies to benefit directly because £1bn of that amount is for procurement.

Our multi-asset thematic portfolio composition at the end of Q1 2026

Investment conclusion

We maintain our defensive positioning with around half of the portfolio in gold or CHF-hedged investments. We have slightly increased our allocation to US equities, focussing on selected thematic opportunities in oversold names. We are increasing our exposure to the UK quantum technologies through a specialist VC fund.

Disclosure

This article represents my personal opinion and is provided for information purposes only. Its content is not intended to be an investment advice, or a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. I use information sources which I believe to be reliable, but their accuracy cannot be guaranteed. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors and, if in doubt, an investor should seek advice from a qualified investment advisor. I am a managing partner of Quantum Exponential, a specialist VC fund.

Related

China’s Stock Market: A Retail Investor’s Guide

China has held the world’s second-largest GDP for over fifteen years, reaching $19.4 trillion by the end of 2025. Only the United States is ahead with $30.6 trillion, and Germany is in third place with $5 trillion. The gap between China and the United States is smaller than the advantage China has over its closest […]

Thematic outlook – where to invest in 2026

Slow and steady (with a little quantum boost) wins the race. Kirill Pyshkin, Mar 02, 2026. Our defensive stance is warranted so far in 2026 In our 2026 investment outlook, we called for overall defensive stance and disclosed that in our multi-asset strategy portfolio roughly half is invested in Gold or hedged to CHF. We also […]

Investment Outlook 2026

Maintain conservative positioning with half portfolio in Gold and Swiss or CHF-hedged assets; equal allocation between bonds/equities. By Kirill Pyshkin Chief Investment Officer of WELREX See this article published on Wealth Briefing We maintain a conservative investment outlook for 2026, characterised by the following positioning: But before we detail our 2026 investment outlook below, we […]

Can Europe afford its rearmament?

WELREX Chief Investment Officer Kirill Pyshkin shares his latest thoughts

TRiUMPh of the Contrarians

WELREX CIO Kirill Pyshkin updates on our 2025 Investment Outlook 3 months on

Robots, relationships and revolutionary investments

WELREX CEO Yevgeni Agerd is interviewed by Yuri Bender and Ali Al Enazi as part of the FT/PWM “Tea Break” series. They discuss the future of wealth management and whether peace talks in Ukraine can spur a much-needed recovery for troubled European economies.

Could 2025 be a better year for thematic equities?

In this article, Kirill Pyshkin, Chief Investment Officer at WELREX, examines whether 2025 could be a better year for thematic funds.

US equities and the dollar deliver a ringing endorsement of Trump. What now?

WELREX Chief Investment Officer, Kirill Pyshkin, offers our investment outlook for 2025 with a non-consensus preference for European vs US assets, including equities, fixed income, and EUR/USD. We like Gold and CHF as a USD inflation hedge but are cautious about commodities.

“Rapid ascent for WELREX – thoughts on business models, Consumer Duty, and more”

Updated WELREX profile published by WealthBriefing following WELREX® Founder and CEO Yevgeni Agerd and Chief Marketing Officer Joe Clift interview with Tom Burroughes, Group Editor.

WELREX included in 2024 WealthTech100 listing

Sixth annual WealthTech100 list names WELREX in their list of companies transforming the world of wealth and asset management.

WELREX joins global elite with double win at WealthBriefing European Awards 2024

At the WealthBriefing European Awards on March 21st, leading wealth management industry participant, WELREX, was selected as a winner in the ‘Innovative Use of Artificial Intelligence’ and ‘Most Promising New Entrant’ categories.

Data, dashboards, and digital wealth

WELREX founder and CEO Yevgeni Agerd speaks to PWM’s editor-in-chief Yuri Bender about the increasing appetite of private investors in developing countries for a hybrid digital and human advice model

Quantum technologies: the next digital revolution

Kirill Pyshkin Investors fear the quantum concept as an unknown quantity, but once they analyse case studies around its transformative nature, it is likely to rival the potential of AI © Envato This article was published in PWM, and FT-affiliate publication, on 14 Nov. 2025 The year 2025 marks a century since quantum mechanics reshaped […]

WELREX CIO, Kirill Pyshkin, invited to present at University of Cambridge

Last week, our Chief Investment Officer, Kirill Pyshkin, led a class of University of Cambridge Master of Finance students at Judge Business School, where he shared his extensive experience in developing and managing thematic investment strategies. Thematic investing, as Kirill explained, is all about identifying the powerful, long-term trends shaping our future and translating them […]