Reflections on our 2025 Investment Outlook three months on.

When Tom Burroughes at Wealth Briefing featured our 2025 Investment Outlook exactly three months ago it looked highly contrarian. It was the market honeymoon after the US elections, the “Trump trade” was in full swing and there seemed to be no alternative to US equities and, in particular, their “Magnificent 7” technology behemoths.

Instead, we argued that US equities will take a breather in 2025 and better returns may be available elsewhere. We suggested equal allocation to equities and bonds but with a preference for Europe over the US. We were concerned about US inflation, and proposed gold, CHF and Bitcoin as a hedge. We were cautious about commodities because we expected that the two active geopolitical conflicts would be settled quickly under Trump. Finally, we predicted that a settlement in Ukraine would act as a strong catalyst for European assets.

Let’s check the reality against those predictions.

Equities

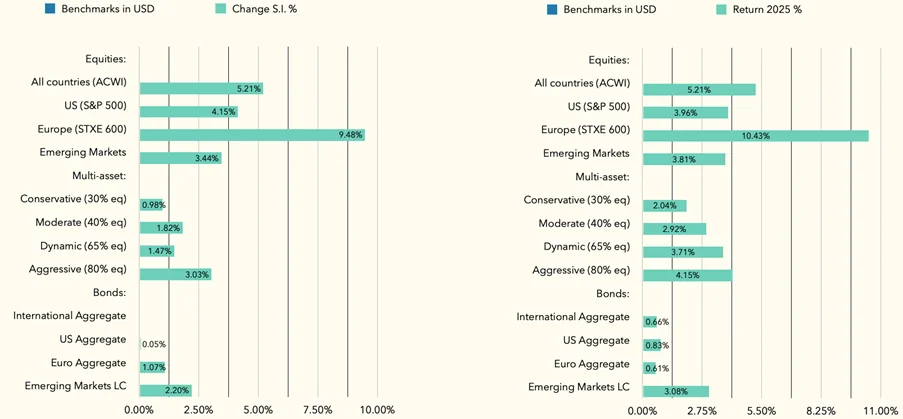

European equities have significantly outperformed US, with the STXE 500 index up 9.5% in USD vs the S&P500 up 4.2% over these three months. In 2025 this outperformance is even stronger with European equities up 10.4% in USD vs US equities up only 4%.

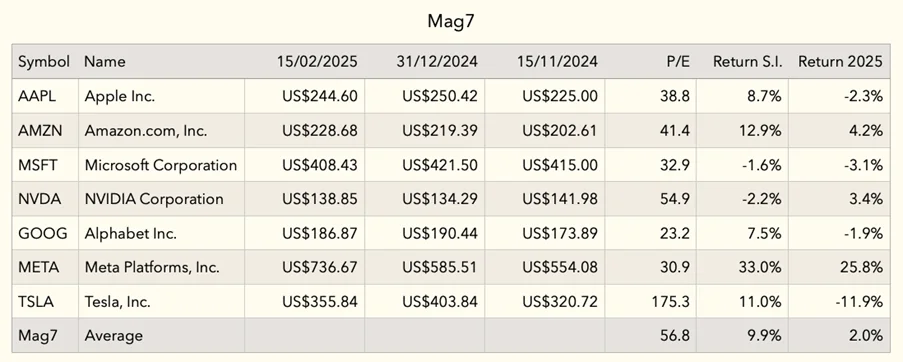

At the same time, the US “Magnificent 7” technology companies have somewhat underwhelmed. Among them, only Meta has maintained its momentum into 2025. Some say that it was the appearance of DeepSeek that unseated the Mag7 leadership. We don’t think so. Rather, we believe that the elevated valuations of the sector were the true reason, and DeepSeek was just a catalyst (note that Tesla is the most expensive and the worst performing in 2025). In the outlook, we specifically warned against the extreme valuations of the US technology sector.

Instead, in the outlook we suggested Chinese equities as a contrarian trade idea. Now, according to the FT, “China’s tech stocks enter bull market after DeepSeek breakthrough”.

The performance of EM equities is almost on par with the US over the last 3 months and even more so in 2025. In our multi-asset portfolio EM equities are the second best-performing bucket, up 9.5% in USD in 2025 (the best performing for us is Gold, which is up 10.8% in USD).

Bonds

There is a similar picture over the 3 months for bonds – US is flat, while European aggregate bonds are up 1.1% in USD. Here, the real surprise is emerging markets’ local currency bonds – up 2.2% in USD over 3 months and 3.1% in 2025. Partially, this may be due to the weakening of the USD against some EM currencies, for example MXN and CNY are a bit stronger against USD, while RUB is 22% stronger vs USD in 2025.

Themes

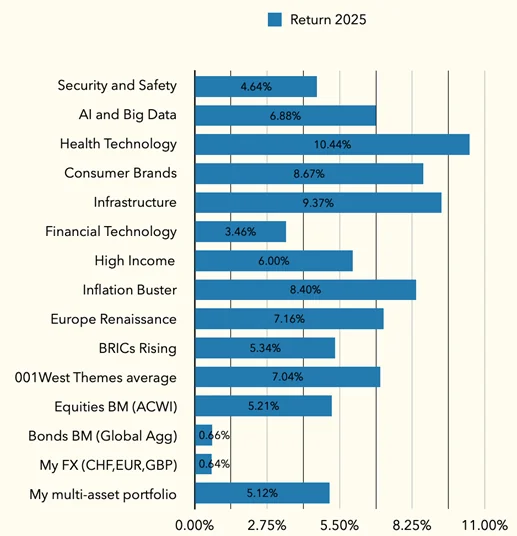

We launched our multi-asset thematic portfolios on 31.12.24 so can only offer an analysis of their performance in 2025. In an article on January 8, we predicted that thematic equities may struggle in 2025 as their performance is negatively correlated with bond yields and we expected yields to stay high. This correlation still holds as yields in the US are down about 10bps YTD and thematics are outperforming. The picture for competitor thematic funds may be less positive because 8 out of 10 of our thematic portfolios are above peer funds that we track in each relevant sector.

Commodities

Oil is down in 2025 but up overall over 3 months. Natural gas is up in double digits given colder weather and no flow through the Ukraine pipeline, meaning that the EU storage is now at its lowest since 2022.

However, as soon as the negotiations on Ukraine were announced, gas prices immediately retreated.

Source: FT https://www.ft.com/content/c2b509b1-79d3-4666-b8a2-e8116a0e7847

In the outlook, we were particularly concerned about the sticky US inflation and suggested Gold as the hedge. Gold was the best performer in our multi-asset portfolio over the 3 months and remained so in 2025. Bitcoin was the other suggestion for those who could stomach its volatility. However, this has only worked since the beginning of 2025 with Bitcoin up by 4.3% in USD, but still down a little (less than 1%) over the 3 months.

Overall, in our portfolio commodities did better than equities both over the last 3 months and in 2025 YTD. Tellingly our “Inflation Buster” thematic multi-asset portfolio containing bonds, equities and commodities is one of the best performing this year, up 8.4% in USD.

Currencies

We controversially expected USD to weaken against a basket of currencies in 2025 despite all the talk of tariffs because tariffs would be an overall negative hit for the US economy if ever implemented in full. Plus longer-term there is a clear shift away from USD in international payments and in central bank reserves.

USD is stronger over the last 3 months but weaker in 2025 against some major DM and EM currencies. For us, EUR, CHF and GBP are of particular importance, and we suggested CHF as another US inflation hedge. Out of those currencies, EUR and CHF strengthened against USD in 2025, but GBP weakened as it is still reeling from the Labour Government budget.

Geopolitical conflicts

In the outlook, we predicted that the geopolitical conflicts will be settled quickly under Trump. The new administration did not disappoint. Trump has imposed his authority with incredible speed, forcing Hamas and Israel into a deal even before his inauguration. We expected this to be negative for oil price, and oil is down.

This week Trump stunned everyone again with a direct call to Putin and starting the Ukraine peace negotiations immediately. We expected this to be negative for oil and gas, and gas in particular has retreated immediately.

We predicted that such a settlement would be a major catalyst for European equities. Now we start to see the evidence of that, for example, see the FT article by (Mari Novik and Arjun Neil Alim) “European stocks rise after Donald Trump signals Ukraine peace talks”.

We continue to believe that the long period of the European assets (including EUR) outperformance is still ahead of us because EU would benefit disproportionally from the end of the conflict in Europe. However, we are carefully watching potentially escalating EU/US trade war given the exchange of unpleasantries during the Munich Security Conference last week.

New ideas

We have now started to rethink the implication of the new realities for European security, including energy security, and made some changes to our portfolio.

Specifically, we reduced allocation to the US defence sector, replacing it with some European defence companies. As the US now insists that the burden of European defence spending should be on Europe, it is only natural to expect that Europeans will try to spend this money domestically.

From the Energy security perspective, the nuclear industry would likely become an even larger part of the European energy mix. Nuclear is where Europe and France in particular has real strength, and we expect further measures to support domestic nuclear champions. Therefore, we added Uranium and other nuclear plays to our commodity mix.

Read the full investment outlook 2025 here:

Kirill Pyshkin, Chief Investment Officer, WELREX, February 2025

Important disclaimer

This article is provided for information purposes only. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation, or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment advisor.

Related

Investment Outlook 2026

Maintain conservative positioning with half portfolio in Gold and Swiss or CHF-hedged assets; equal allocation between bonds/equities. By Kirill Pyshkin Chief Investment Officer of WELREX We maintain a conservative investment outlook for 2026, characterised by the following positioning: But before we detail our 2026 investment outlook below, we would like to review the final performance […]

Quantum technologies: the next digital revolution

Kirill Pyshkin Investors fear the quantum concept as an unknown quantity, but once they analyse case studies around its transformative nature, it is likely to rival the potential of AI © Envato This article was published in PWM, and FT-affiliate publication, on 14 Nov. 2025 The year 2025 marks a century since quantum mechanics reshaped […]

Can Europe afford its rearmament?

WELREX Chief Investment Officer Kirill Pyshkin shares his latest thoughts

Robots, relationships and revolutionary investments

WELREX CEO Yevgeni Agerd is interviewed by Yuri Bender and Ali Al Enazi as part of the FT/PWM “Tea Break” series. They discuss the future of wealth management and whether peace talks in Ukraine can spur a much-needed recovery for troubled European economies.

Could 2025 be a better year for thematic equities?

In this article, Kirill Pyshkin, Chief Investment Officer at WELREX, examines whether 2025 could be a better year for thematic funds.

US equities and the dollar deliver a ringing endorsement of Trump. What now?

WELREX Chief Investment Officer, Kirill Pyshkin, offers our investment outlook for 2025 with a non-consensus preference for European vs US assets, including equities, fixed income, and EUR/USD. We like Gold and CHF as a USD inflation hedge but are cautious about commodities.

“Rapid ascent for WELREX – thoughts on business models, Consumer Duty, and more”

Updated WELREX profile published by WealthBriefing following WELREX® Founder and CEO Yevgeni Agerd and Chief Marketing Officer Joe Clift interview with Tom Burroughes, Group Editor.

WELREX included in 2024 WealthTech100 listing

Sixth annual WealthTech100 list names WELREX in their list of companies transforming the world of wealth and asset management.

WELREX joins global elite with double win at WealthBriefing European Awards 2024

At the WealthBriefing European Awards on March 21st, leading wealth management industry participant, WELREX, was selected as a winner in the ‘Innovative Use of Artificial Intelligence’ and ‘Most Promising New Entrant’ categories.

Data, dashboards, and digital wealth

WELREX founder and CEO Yevgeni Agerd speaks to PWM’s editor-in-chief Yuri Bender about the increasing appetite of private investors in developing countries for a hybrid digital and human advice model

WELREX CIO, Kirill Pyshkin, invited to present at University of Cambridge

Last week, our Chief Investment Officer, Kirill Pyshkin, led a class of University of Cambridge Master of Finance students at Judge Business School, where he shared his extensive experience in developing and managing thematic investment strategies. Thematic investing, as Kirill explained, is all about identifying the powerful, long-term trends shaping our future and translating them […]

Strong 1H 2025 Performance of Our Thematic Investment Strategies

In a financial landscape constantly reshaped by powerful global forces, understanding and responding to long-term trends is paramount. At WELREX, we believe in a proactive approach to investment, rooted in deep thematic analysis and a multi-asset strategy designed to navigate complex markets. As we reflect on the first half of 2025, our Chief Investment Officer, […]

US Treasuries deserve another look

The recent escalation in the Israel-Iran conflict has sharpened investor focus on the relationship between oil prices and financial markets. While the typical ‘risk-off’ response—favouring bonds and pressuring equities—is well understood during periods of geopolitical tension, the implications of rising oil prices are more nuanced. Moreover, most economists speak in unison about their overwhelming belief that Trump’s […]