We’d rather see infrastructure investments.

Excerpts from this perspective were featured in a Wealth Briefing article on March 12th 2025.

The memorable speech by JD Vance at the Munich Security Conference has spurred European leaders into action. It has become clear that the US may no longer extend its security guarantee to Europe.

An outburst of activity has followed. Spearheaded by the President of France, the UK Prime Minister. and Chancellor-Elect of Germany, Europeans are searching for new ways to guarantee their security.

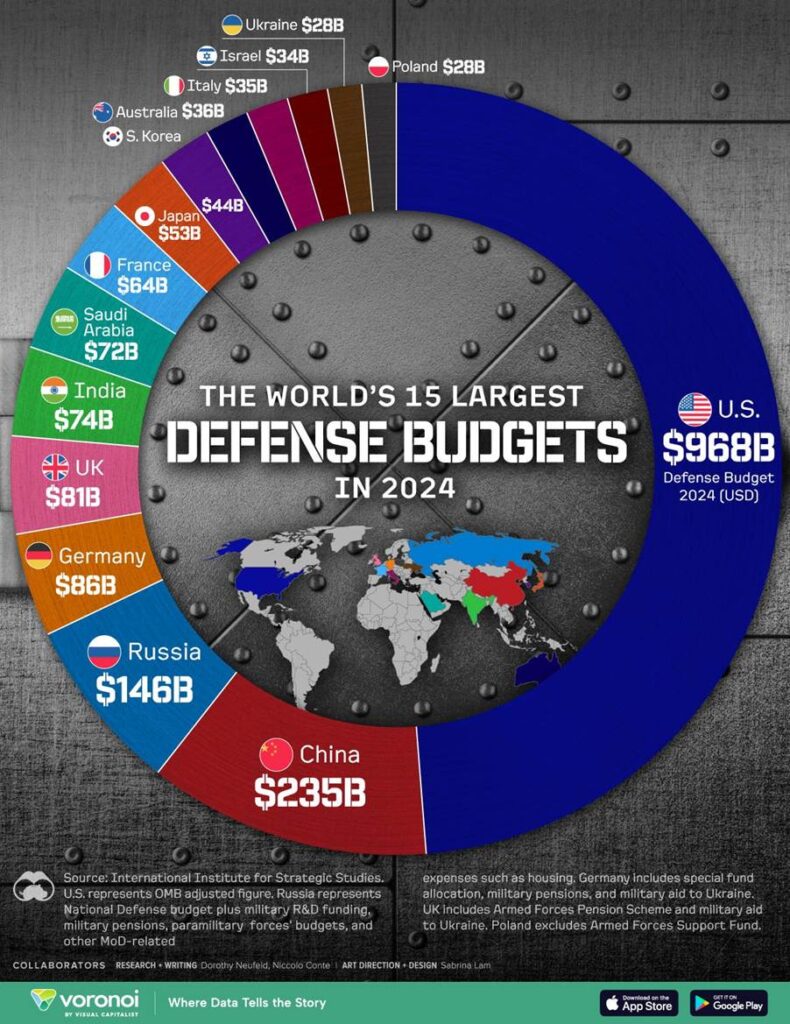

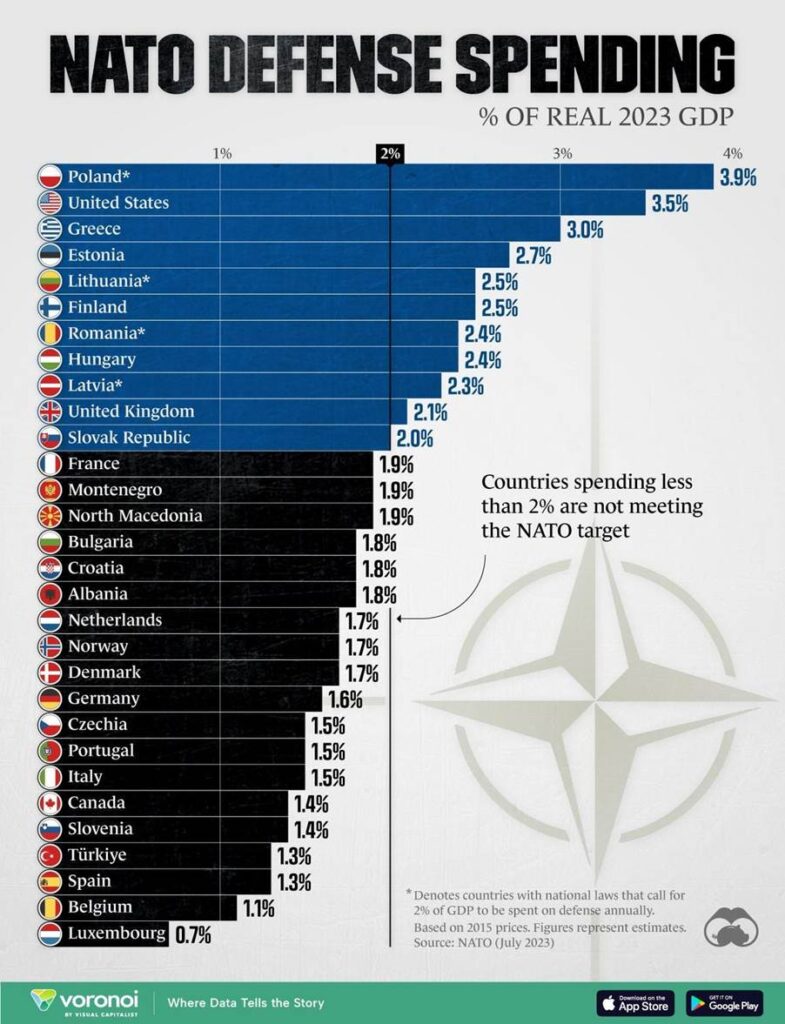

The US spends $968bn on defence or 3.5% of its GDP, which accounts for over half of the total NATO budget. The next biggest European spenders in NATO are Germany with $86bn (1.6% of GDP), the UK $81bn (2.1% of GDP), and France $64bn (1.9% of GDP).

Source: https://www.visualcapitalist.com/largest-defense-budgets-in-the-world/

Therefore, it would be very difficult, if not impossible, to fill the gap left by the US in NATO. The three biggest European spenders – UK, Germany and France – did not even account for 1/4 of the US spending in 2024.

Let’s take France, which has roughly the same budget deficit as the US at just over 6%. If France were going to increase its spending on defence from 1.9% to 5%, as requested by Trump, its deficit would exceed 9%, an unacceptable amount.

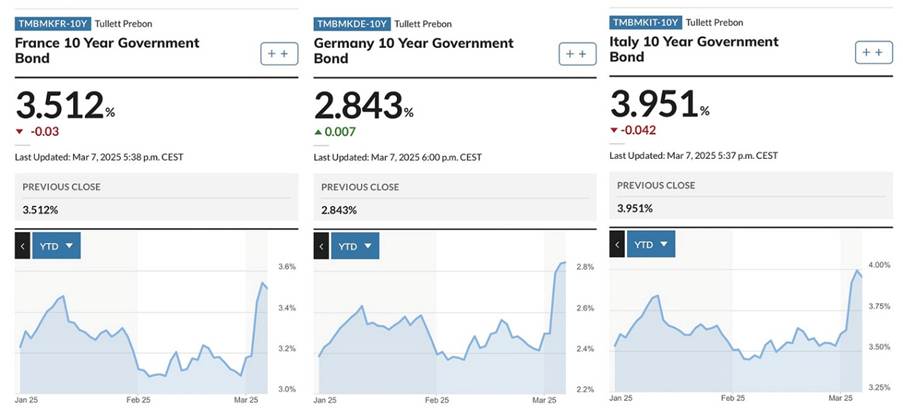

In fact, any additional spending is already too much. French 10-year Government bond yield jumped last week by 40bps, to over 3.5%. Given the French public debt of EUR 3.3trln or 114% of GDP, an increase of 40bps would account for an extra EUR 13bn of interest, which is equivalent to an additional 20% of the French defence spending in 2024.

Italian 10-year yields also spiked by 40bps to 3.95%. With the EUR 3trln public debt of Italy, representing an even higher 119% of GDP, an additional 40bps of interest is equivalent to EUR 12bn, or over 1/3 of Italian defence spending in 2024.

German yields spiked by over 40bps to above 2.8% last week. Last Wednesday and Thursday was the largest two-day sell-off in German government bonds since the 1970s.

Source: Trading Economics

That means that just a DISCUSSION of more defence spending can increase the ACTUAL cash spending by an amount equivalent to 20-35% of the current defence spending through an increase in debt servicing cost. So, if the defence spending in those countries rose to 5% of GDP, that would not only increase the budget deficit by half, as in France but also explode the interest paid on public debt.

When four months ago we recommended Eurozone bonds in our investment outlook for 2025, we did not foresee an increase in the fiscal deficit in the EU, instead, we commended the progress made after the Eurozone crisis.

Yes, this will benefit to certain sectors of the economy. On Feb.16 we already suggested European defence equities as a trade idea, because it is only natural to expect Europeans to spend their money on defence at home. EUAD, a European defence ETF, is up by 39% in USD year to date.

But we very much prefer the idea of Friedrich Merz increasing infrastructure spending. Unlike nuclear warheads, which hopefully would never be used, infrastructure investments have long-term benefits and are a foundation for sustained economic growth and development. For example, Germany could restart its nuclear power plants, securing lower energy electricity prices for industry, thus improving its competitiveness. (We also recommended nuclear as an investment theme on Feb 16).

In conclusion, we prefer to see infrastructure rather than defence investments in Europe as that would ensure long-term competitiveness of the economy. In contrast, defence will only provide a short-term boost to certain sectors but may increase the borrowing costs, negating the benefit.

Kirill Pyshkin, Chief Investment Officer, WELREX, March 2025

Important disclaimer

This article is provided for information purposes only. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation, or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment advisor.

Related

War and Peace

How does the war in the Middle East impact our investment outlook plus Q1 2026 portfolio and thematic review Kirill Pyshkin Apr 12, 2026 Source: The Economist cover 09.04.2026 edition The super defensive stance that we advocated at the beginning of this year in our 2026 investment outlook with half of our portfolio invested in gold or hedged to […]

China’s Stock Market: A Retail Investor’s Guide

China has held the world’s second-largest GDP for over fifteen years, reaching $19.4 trillion by the end of 2025. Only the United States is ahead with $30.6 trillion, and Germany is in third place with $5 trillion. The gap between China and the United States is smaller than the advantage China has over its closest […]

Thematic outlook – where to invest in 2026

Slow and steady (with a little quantum boost) wins the race. Kirill Pyshkin, Mar 02, 2026. Our defensive stance is warranted so far in 2026 In our 2026 investment outlook, we called for overall defensive stance and disclosed that in our multi-asset strategy portfolio roughly half is invested in Gold or hedged to CHF. We also […]

Investment Outlook 2026

Maintain conservative positioning with half portfolio in Gold and Swiss or CHF-hedged assets; equal allocation between bonds/equities. By Kirill Pyshkin Chief Investment Officer of WELREX See this article published on Wealth Briefing We maintain a conservative investment outlook for 2026, characterised by the following positioning: But before we detail our 2026 investment outlook below, we […]

TRiUMPh of the Contrarians

WELREX CIO Kirill Pyshkin updates on our 2025 Investment Outlook 3 months on

Robots, relationships and revolutionary investments

WELREX CEO Yevgeni Agerd is interviewed by Yuri Bender and Ali Al Enazi as part of the FT/PWM “Tea Break” series. They discuss the future of wealth management and whether peace talks in Ukraine can spur a much-needed recovery for troubled European economies.

Could 2025 be a better year for thematic equities?

In this article, Kirill Pyshkin, Chief Investment Officer at WELREX, examines whether 2025 could be a better year for thematic funds.

US equities and the dollar deliver a ringing endorsement of Trump. What now?

WELREX Chief Investment Officer, Kirill Pyshkin, offers our investment outlook for 2025 with a non-consensus preference for European vs US assets, including equities, fixed income, and EUR/USD. We like Gold and CHF as a USD inflation hedge but are cautious about commodities.

“Rapid ascent for WELREX – thoughts on business models, Consumer Duty, and more”

Updated WELREX profile published by WealthBriefing following WELREX® Founder and CEO Yevgeni Agerd and Chief Marketing Officer Joe Clift interview with Tom Burroughes, Group Editor.

WELREX included in 2024 WealthTech100 listing

Sixth annual WealthTech100 list names WELREX in their list of companies transforming the world of wealth and asset management.

WELREX joins global elite with double win at WealthBriefing European Awards 2024

At the WealthBriefing European Awards on March 21st, leading wealth management industry participant, WELREX, was selected as a winner in the ‘Innovative Use of Artificial Intelligence’ and ‘Most Promising New Entrant’ categories.

Data, dashboards, and digital wealth

WELREX founder and CEO Yevgeni Agerd speaks to PWM’s editor-in-chief Yuri Bender about the increasing appetite of private investors in developing countries for a hybrid digital and human advice model

Quantum technologies: the next digital revolution

Kirill Pyshkin Investors fear the quantum concept as an unknown quantity, but once they analyse case studies around its transformative nature, it is likely to rival the potential of AI © Envato This article was published in PWM, and FT-affiliate publication, on 14 Nov. 2025 The year 2025 marks a century since quantum mechanics reshaped […]